Abstract

The banking industry has undergone a substantial transformation in recent years due to the rapid digitization of financial services, increasing cyber threats, and evolving customer expectations for seamless digital experiences. Traditional password-based security mechanisms have proven insufficient against sophisticated cyberattacks such as phishing, credential stuffing, identity theft, account takeover fraud, and social engineering. Consequently, financial institutions have increasingly adopted biometric security and advanced authentication mechanisms to strengthen cybersecurity frameworks while maintaining user convenience. This scholarly article examines the evolution, implementation, and significance of biometric authentication technologies within the banking industry, including fingerprint recognition, facial recognition, voice biometrics, behavioral biometrics, multi-factor authentication (MFA), adaptive authentication, and artificial intelligence-driven fraud prevention systems. The article further explores the balance between security and usability, regulatory compliance considerations, privacy challenges, and the future role of biometric authentication in digital banking ecosystems. The findings demonstrate that biometric and advanced authentication systems significantly enhance banking security infrastructures while simultaneously improving customer experience, operational efficiency, and fraud detection capabilities.

Introduction

The global banking sector has become one of the most targeted industries for cybercriminals due to the enormous volume of sensitive financial data processed daily. As banking services increasingly migrate toward digital and mobile platforms, financial institutions face mounting pressure to protect customer accounts from evolving cybersecurity threats without introducing friction that may negatively impact user experience. Historically, banks relied heavily on password-based authentication systems, security questions, and PIN verification methods. However, these conventional approaches are vulnerable to hacking, phishing attacks, credential theft, brute-force attacks, and human error.

The growing complexity of cyber threats has accelerated the adoption of biometric security and advanced authentication technologies across banking ecosystems. Biometric authentication uses unique physiological or behavioral characteristics such as fingerprints, facial features, iris patterns, voiceprints, and typing behaviors to verify user identity. These technologies offer stronger identity assurance because biometric traits are inherently difficult to replicate or steal compared to traditional passwords.

In parallel, advanced authentication mechanisms such as multi-factor authentication, risk-based authentication, adaptive authentication, device intelligence, and artificial intelligence-powered fraud analytics have emerged as critical components of modern banking cybersecurity strategies. These technologies enable banks to deliver secure yet frictionless customer experiences by intelligently evaluating risk levels in real time and dynamically adjusting authentication requirements accordingly.

The integration of biometric security solutions within banking systems reflects a broader industry shift toward customer-centric cybersecurity models that prioritize both protection and convenience. Customers increasingly expect instant access to banking services through mobile applications, online platforms, digital wallets, and contactless payment systems. Financial institutions must therefore implement security solutions that safeguard accounts while minimizing login complexity and transaction delays.

This article provides a comprehensive analysis of biometric security and advanced authentication mechanisms within the banking industry, their operational significance, technological advancements, benefits, challenges, and long-term implications for financial cybersecurity.

Evolution of Authentication Mechanisms in Banking

Authentication mechanisms within the banking industry have evolved significantly over the past several decades. Early banking systems primarily relied on physical identity verification through handwritten signatures, paper documentation, and in-person interactions. With the rise of automated teller machines (ATMs), banks introduced PIN-based authentication systems that enabled customers to access financial services electronically.

The expansion of internet banking during the late 1990s and early 2000s introduced username-password authentication frameworks. Although passwords initially provided a convenient method for securing online accounts, they quickly became vulnerable to cyberattacks. Weak password practices, password reuse across multiple platforms, and phishing scams contributed to a dramatic increase in account compromise incidents.

To address these vulnerabilities, banks implemented two-factor authentication systems involving one-time passwords (OTPs), SMS verification codes, hardware tokens, and email-based verification mechanisms. While these approaches improved security, they often introduced customer inconvenience and were themselves susceptible to SIM-swapping attacks, interception, and phishing.

The emergence of smartphones, mobile banking applications, and advanced biometric sensors transformed the authentication landscape. Modern mobile devices now include fingerprint scanners, facial recognition systems, secure enclaves, and behavioral analytics capabilities that allow banks to authenticate users more securely and efficiently.

Today, banking authentication systems are increasingly powered by artificial intelligence, machine learning, and behavioral analytics that continuously assess user risk profiles in real time. Rather than relying solely on static credentials, modern authentication mechanisms dynamically evaluate contextual factors such as device location, transaction behavior, login patterns, and user biometrics to determine authentication requirements.

Biometric Authentication Technologies in Banking

Fingerprint Recognition

Fingerprint authentication has become one of the most widely adopted biometric technologies within the banking industry. Mobile banking applications commonly integrate fingerprint authentication using embedded smartphone sensors to enable secure login access and transaction approvals.

Fingerprint biometrics offer several advantages, including convenience, speed, and uniqueness. Unlike passwords, fingerprints cannot easily be forgotten or shared. Additionally, modern fingerprint recognition systems utilize encrypted biometric templates stored within secure hardware environments, reducing the risk of credential theft.

Banks use fingerprint authentication to secure mobile banking access, ATM transactions, payment authorizations, and digital wallet integrations. The implementation of fingerprint-based authentication has significantly reduced dependency on passwords and improved customer satisfaction by enabling faster authentication experiences.

Facial Recognition

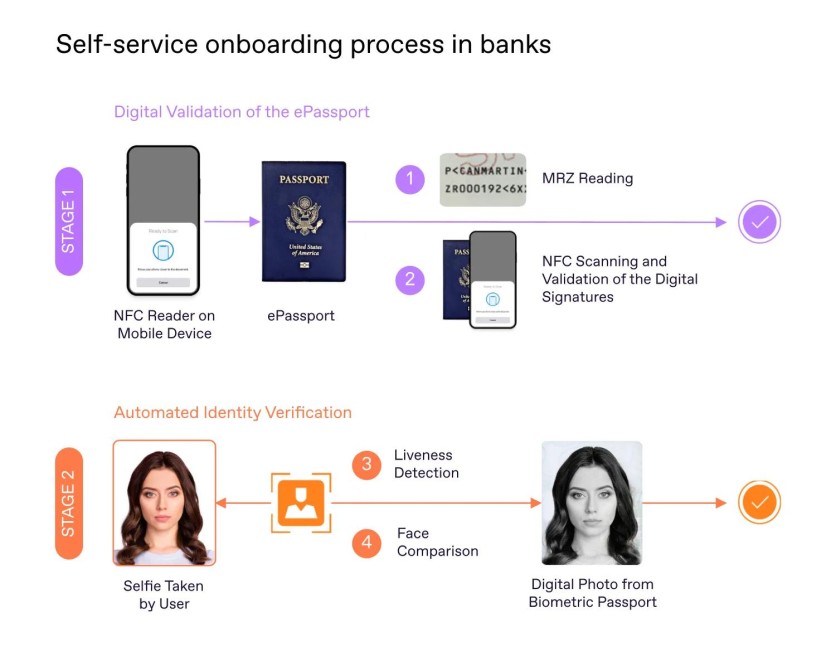

Facial recognition technology has rapidly gained prominence within banking security infrastructures. Banks use facial recognition for customer onboarding, remote identity verification, fraud prevention, and mobile banking authentication.

Facial biometrics leverage artificial intelligence and computer vision algorithms to analyze facial structures and compare them against stored biometric templates. Advanced facial recognition systems include liveness detection capabilities that prevent spoofing attacks using photographs, videos, or masks.

The adoption of facial recognition has been particularly valuable in digital account opening processes where customers can remotely verify their identities without visiting physical bank branches. This capability has enhanced operational efficiency while expanding access to financial services.

Voice Biometrics

Voice biometrics analyzes unique vocal characteristics such as pitch, tone, speech patterns, and pronunciation to authenticate users. Financial institutions increasingly deploy voice authentication systems within customer service call centers to improve identity verification processes.

Traditional call center authentication procedures often required customers to answer multiple security questions, creating lengthy and frustrating interactions. Voice biometrics streamlines this process by enabling passive authentication during natural conversation, thereby reducing call handling times and enhancing customer experience.

Voice biometric systems also strengthen fraud detection capabilities by identifying suspicious voice patterns, synthetic speech attempts, and impersonation attacks.

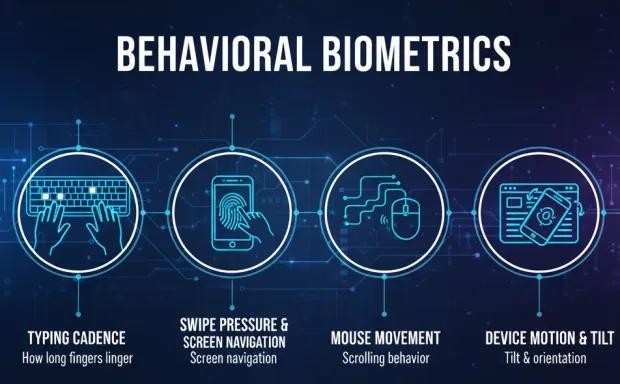

Behavioral Biometrics

Behavioral biometrics represent one of the most innovative developments in banking cybersecurity. Unlike physiological biometrics, behavioral biometrics analyze patterns in user behavior such as typing speed, touchscreen pressure, mouse movements, device handling, navigation habits, and transaction behavior.

Behavioral biometric systems continuously authenticate users in the background without requiring active customer participation. This passive authentication approach significantly improves usability while enhancing fraud prevention.

Machine learning algorithms analyze behavioral deviations that may indicate account takeover attempts or fraudulent activity. For example, if a user suddenly logs in from an unfamiliar device and demonstrates abnormal typing behavior, the system may trigger additional authentication requirements or temporarily block access.

Behavioral biometrics are especially valuable because they provide continuous authentication rather than one-time verification at login.

Advanced Authentication Mechanisms

Multi-Factor Authentication (MFA)

Multi-factor authentication combines multiple verification factors, typically including:

- Something the user knows (password or PIN)

- Something the user has (mobile device or hardware token)

- Something the user is (biometric identifier)

MFA significantly enhances banking security by requiring attackers to compromise multiple authentication layers simultaneously. Modern banking systems increasingly integrate biometrics within MFA frameworks to strengthen identity assurance while minimizing user friction.

Banks commonly deploy MFA for high-risk transactions such as wire transfers, large withdrawals, password resets, and cross-border payments.

Adaptive Authentication

Adaptive authentication uses contextual intelligence and risk-based analysis to dynamically determine authentication requirements based on transaction risk levels. Rather than applying uniform authentication procedures to all users and activities, adaptive systems evaluate multiple factors, including:

- Geolocation

- Device reputation

- Login time

- Transaction history

- Behavioral patterns

- Network characteristics

Low-risk activities may require minimal authentication, while high-risk scenarios trigger additional verification measures. This intelligent approach improves security without unnecessarily burdening legitimate customers.

Artificial Intelligence and Machine Learning

Artificial intelligence has become central to modern banking authentication systems. AI-driven fraud detection platforms analyze vast amounts of transactional and behavioral data to identify suspicious patterns in real time.

Machine learning algorithms continuously improve authentication accuracy by learning from evolving fraud techniques and user behavior. These systems can detect anomalies such as impossible travel patterns, unusual spending activity, bot-driven attacks, and synthetic identity fraud.

AI-powered authentication systems also reduce false positives, minimizing unnecessary account lockouts and improving customer trust.

Benefits of Biometric Security in Banking

Enhanced Security

Biometric authentication significantly reduces reliance on passwords, which are among the weakest elements in cybersecurity infrastructures. Since biometric traits are difficult to replicate or steal, biometric systems provide stronger identity verification.

Additionally, advanced authentication systems reduce the success rate of phishing attacks, credential stuffing, and social engineering schemes.

Improved Customer Experience

One of the primary advantages of biometric authentication is convenience. Customers can access accounts quickly using fingerprints or facial recognition rather than remembering complex passwords or waiting for OTP verification codes.

The reduction in authentication friction contributes to higher customer satisfaction and increased adoption of digital banking services.

Fraud Reduction

Biometric and AI-driven authentication systems enhance fraud detection by continuously monitoring user activity and identifying suspicious behavior patterns. Financial institutions using behavioral biometrics and machine learning analytics can detect account takeover attempts earlier and respond more effectively.

Operational Efficiency

Automated biometric authentication streamlines customer onboarding, transaction approval, and call center verification processes. This reduces operational costs associated with manual identity verification and customer support interactions.

Banks can also accelerate digital transformation initiatives by enabling secure remote banking services.

Challenges and Privacy Concerns

Despite their advantages, biometric authentication systems present several challenges that financial institutions must address.

Data Privacy and Security

Biometric data is highly sensitive because it is permanent and cannot easily be changed if compromised. Banks must implement robust encryption, secure storage mechanisms, and strict access controls to protect biometric templates.

Regulatory frameworks such as the General Data Protection Regulation (GDPR) and various financial privacy laws impose strict requirements regarding biometric data collection, processing, and storage.

Spoofing and Deepfake Threats

Cybercriminals increasingly use advanced technologies such as deepfakes, synthetic voices, and AI-generated facial replicas to bypass biometric systems. Banks must therefore invest in liveness detection, anti-spoofing algorithms, and continuous authentication technologies.

Ethical and Regulatory Challenges

The use of biometric surveillance and behavioral monitoring raises ethical concerns regarding consent, transparency, and user privacy. Financial institutions must maintain clear policies explaining how biometric data is used and ensure compliance with evolving regulations.

Accessibility Concerns

Certain biometric technologies may not function effectively for all users. For example, facial recognition systems may experience accuracy disparities under varying lighting conditions, while fingerprint recognition may not work for individuals with damaged fingerprints.

Banks must therefore provide alternative authentication methods to ensure inclusivity and accessibility.

Future Trends in Banking Authentication

The future of banking authentication will likely involve increasingly sophisticated combinations of biometrics, artificial intelligence, decentralized identity systems, and passwordless authentication architectures.

Emerging technologies such as decentralized digital identities, blockchain-based identity verification, and continuous authentication systems may further transform banking cybersecurity models. Additionally, advancements in quantum-resistant cryptography may become essential as quantum computing evolves.

Behavioral biometrics and AI-driven adaptive authentication are expected to become more prominent as banks seek to reduce authentication friction while strengthening fraud prevention capabilities.

The convergence of biometric authentication with wearable devices, Internet of Things (IoT) ecosystems, and embedded finance platforms will also expand the role of biometric security beyond traditional banking applications.

Conclusion

Biometric security and advanced authentication mechanisms have become fundamental components of modern banking cybersecurity strategies. As digital banking adoption continues to accelerate, financial institutions must balance robust security measures with seamless customer experiences.

Biometric technologies such as fingerprint recognition, facial recognition, voice biometrics, and behavioral analytics provide significantly stronger identity verification capabilities compared to traditional password-based systems. Simultaneously, advanced authentication mechanisms, including multi-factor authentication, adaptive authentication, and AI-powered fraud detection, enable banks to dynamically respond to evolving cyber threats.

The integration of these technologies not only enhances account security but also improves customer convenience, operational efficiency, and fraud prevention effectiveness. However, financial institutions must carefully address privacy concerns, regulatory compliance obligations, ethical considerations, and emerging threats such as deepfakes and biometric spoofing attacks.

Ultimately, biometric security and advanced authentication mechanisms represent a transformative advancement in banking cybersecurity. Their continued evolution will play a critical role in shaping the future of secure, customer-centric digital banking ecosystems while enabling financial institutions to maintain trust, resilience, and competitiveness in an increasingly digital financial landscape.

ⓒ 2026 TECHTIMES.com All rights reserved. Do not reproduce without permission.