Intel (Nasdaq: INTC) climbed about 8.55% on Monday, June 8, 2026, after a cluster of analyst price-target increases and a run of AI-infrastructure deals recast the long-struggling chipmaker as a credible contender in the data-center build-out. The jump extends one of the year's most volatile large-cap turnaround trades: the stock swung from the $120–126 zone in late May down into the high $90s, then rebounded back above $107 on the latest news.

For an investor deciding what to do with INTC now, the move matters because it is not a single headline — it is the market re-rating an entire thesis at once, while the company's actual financials still lag the story the stock is telling.

Why Are Analysts Raising Intel Price Targets Now?

Three brokerages lifted their Intel targets into Monday's session. Wells Fargo moved its target from $85 to $110, citing stronger-than-expected AI data-center demand and incremental server-CPU demand from fast-growing agentic AI workloads. Barclays raised its target from $65 to $100, pointing to rising AI CPU demand even while still favoring rival AMD overall. Mizuho went further, to $128. The consensus target still sits near the mid-$90s — the tell that Wall Street is warming to Intel's AI narrative without yet being all-in.

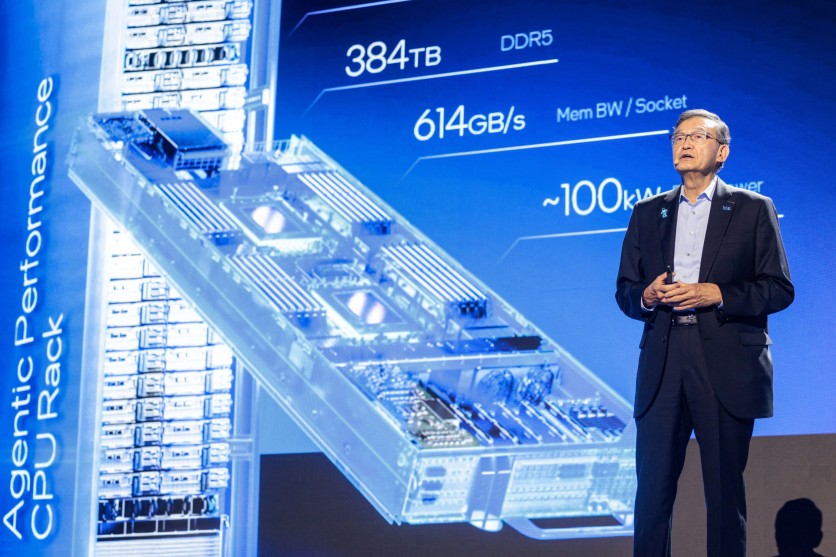

The catalyst is a deliberate repositioning. At Computex 2026, Intel stopped presenting as a CPU vendor and pitched itself as a full-stack AI infrastructure provider: rackscale systems pairing its processors with SambaNova's reconfigurable dataflow units, a role in a new disaggregated inference cloud, and its first data-center CPUs on the 18A process node. That is the kind of multi-year story that can support an elevated multiple — if execution follows.

What Is Intel's Full-Stack AI Strategy Built On?

The hardware gives the narrative substance. Intel's Xeon 6+ "Clearwater Forest" is its first data-center CPU on the 18A node, packing as many as 288 efficiency cores into a single socket and shipping immediately through tier-one server vendors. After years of manufacturing setbacks and a closely watched turnaround under CEO Lip-Bu Tan, a flagship part built on Intel's most advanced node — available the day it was announced — is the most concrete proof yet that 18A is a real product line rather than a roadmap promise.

Intel is also competing on economics rather than raw performance alone. Its Crescent Island inference accelerator, planned for late 2026, uses LPDDR5x memory and air cooling to target cost-sensitive and potentially China-compliant workloads, and a separate year-end AI data-center chip aims directly at Nvidia and AMD with cheaper memory and cooling to undercut total cost of ownership. Neither moves the current quarter's earnings, but together they extend a roadmap analysts are using to justify an AI-style valuation.

👉 Read more:

Intel Xeon 6 Plus Clearwater Forest Launches: 288 Cores, 18A Node Hits Data Center

Intel Crescent Island GPU Packs 480GB Without HBM: Xe3P Targets Inference Gap

How Do the SambaNova and Foxconn Deals Fit Together?

Beyond silicon, Intel has been signing partners that widen its reach. A strategic collaboration with Foxconn to co-develop next-generation AI infrastructure and edge platforms drove a roughly 4.4% premarket pop, as traders bet that pairing Intel's silicon and software with Foxconn's manufacturing scale could push AI systems into data centers and physical-AI deployments faster. Intel and 3DGS plan to invest about $3.3 billion in an advanced packaging plant in India, expanding glass-core and high-density substrate capacity — and advanced packaging and power efficiency are genuine bottlenecks in AI hardware, not cosmetic ones. A separate collaboration with Hitachi targets physical AI, factory automation, and energy optimization.

The SambaNova tie-up is the load-bearing one for the AI pitch: it lets Intel sell a complete rack — its CPUs orchestrating SambaNova's dataflow accelerators for inference — rather than a single chip a buyer must integrate. That is what "full-stack" means in practice, and it is the difference between competing for a server slot and competing for a data-center contract.

Do Intel's Fundamentals Justify the Move?

For all the momentum, Intel remains a turnaround in progress, and the numbers show it. Revenue over the trailing year sits around $52.9 billion, but profitability is thin to negative: profit margin near -6%, return on equity slightly below zero, and free cash flow of roughly -$2.54 billion in the latest quarter. The balance sheet is sturdier, with a current ratio of 2.3 and total debt to equity of just 0.4, giving the company room to fund its rebuild.

Valuation is where the debate sharpens. INTC trades at a price-to-sales ratio near 8.8 and above 40 times forward earnings — a multiple that, as one widely circulated note observed, towers over memory maker Micron's roughly 9 times. A great deal of AI optimism is already in the price. The stock is being valued as a high-growth AI story, not the cyclical value play it was a year ago, which raises the bar for the execution that has to come next. Encouragingly, commentary from the Bank of America technology conference suggested some 2027 margin goals could be reached or pulled forward — the single variable that matters most to the bull case.

Is Intel Stock a Buy in 2026?

The bull case: Intel now has shipping 18A silicon, a full-stack pitch with named partners, a roadmap built around total cost of ownership rather than a losing fight on raw performance, and a Street raising targets toward and above $110. If 18A yields hold, the SambaNova and Foxconn collaborations convert to volume, and 2027 margins pull forward, the current multiple becomes easier to defend.

The bear case: Intel is still unprofitable on several measures, free cash flow is negative, and above 40 times forward earnings the stock already embeds a turnaround that has not reached the income statement. Barclays, even after raising its target, still prefers AMD. Supply is tight — Intel has said 18A allocation is managed "daily, in some cases," a sign of demand but also of execution risk — and the next-generation Xeon 7 "Diamond Rapids" is not due until 2027, so the proof points investors most want are still quarters away.

The catalysts to watch over the next two quarters are concrete: 18A production yields and allocation, whether the year-end AI data-center chip and Crescent Island ship on schedule, and whether margins move toward the pulled-forward 2027 targets. This article is not investment advice.

👉 Read more:

Why Big Tech Is Pouring Billions Into AI Data Centers and Reinventing Tech Infrastructure

Frequently Asked Questions

Why did Intel stock jump on June 8, 2026?

Intel rose about 8.55% after Wells Fargo, Barclays, and Mizuho raised their price targets and the company unveiled a full-stack AI infrastructure strategy at Computex 2026. New collaborations with SambaNova and Foxconn, plus a planned $3.3 billion advanced-packaging plant in India, reinforced the view that Intel is a real participant in the AI data-center build-out.

What are the latest Intel price targets?

Wells Fargo raised its target to $110 from $85, Barclays to $100 from $65, and Mizuho to $128. The consensus target still sits near the mid-$90s, indicating Wall Street is growing more positive but remains divided on how much of Intel's AI turnaround is already priced in.

Is Intel stock a good buy in 2026?

Analysts are increasingly constructive, with targets ranging from roughly $100 to $128 against recent prices near $107. The bull case rests on shipping 18A silicon, the SambaNova and Foxconn deals, and potential 2027 margin gains; the main risks are Intel's negative free cash flow, a forward multiple above 40 times earnings, and execution risk on 18A supply. This article does not constitute investment advice.

What is Intel's 18A process and why does it matter?

18A is Intel's most advanced manufacturing node and the basis for its Xeon 6+ "Clearwater Forest" data-center CPUs, which ship with up to 288 efficiency cores. After years of delays, shipping 18A hardware through tier-one server vendors is the clearest evidence that Intel's manufacturing turnaround under CEO Lip-Bu Tan is producing real products rather than roadmap promises.

ⓒ 2026 TECHTIMES.com All rights reserved. Do not reproduce without permission.