The AI infrastructure boom has created its next supply chain crisis. Having already driven shortages in GPUs, high-bandwidth memory, and advanced packaging substrates, the relentless buildout of AI data centers has now produced a severe crunch in optical communications components — the high-speed lasers, fiber optic cables, and transceivers that form the nervous system connecting racks inside AI training clusters. A Nikkei Asia report published Tuesday confirmed the shortage is global, prices are rising, and the crisis is expected to persist well into 2027.

According to McKinsey analysis, production of 800-gigabit-per-second transceivers will fall 40 to 60 percent short of demand through 2027, with shortfalls of 30 to 40 percent likely for 1.6-terabit-per-second devices through 2029. The numbers reflect a structural manufacturing constraint, not a cyclical inventory correction — and a single strategic decision by Nvidia has made it significantly worse for everyone else.

57% Market Surge, Supply Nowhere Near to Match

Research firm TrendForce projects the global market for AI-focused optical transceivers will expand from $16.5 billion in 2025 to $26 billion in 2026 — growth of more than 57% year-over-year. Shipments of 800G and higher transceivers, the workhorses of modern AI cluster interconnects, are forecast to surge from 24 million units in 2025 to nearly 63 million in 2026 — a 2.6-fold jump in a single year.

Traffic at hyperscale data centers in North America has sustained over 30% annual growth, prompting cloud giants including Google, Microsoft, and Meta to accelerate GPU and AI server deployment, which has in turn driven record procurement of high-speed optical interconnects. The narrative in markets tracks in precise sequence: 2024 was defined by GPU shortages, 2025 by memory and high-bandwidth memory — and 2026 by optical components.

Nvidia Locks Up EML Laser Supply, Pushing Competitors Past 2027

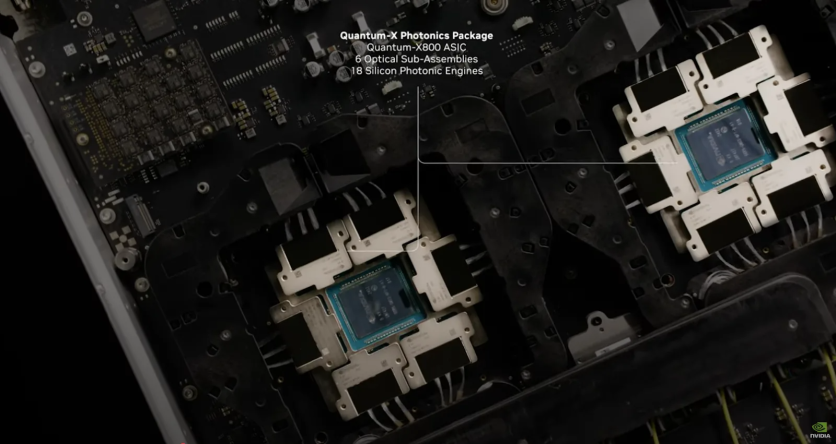

At the heart of the crisis is a small, technically demanding component called the electro-absorption modulated laser, or EML. An EML combines a continuous light source and a high-speed modulator on a single chip, encoding data onto light signals traveling through fiber optic cable at speeds up to 200 gigabits per lane. EMLs are essential for the high-speed transceivers that connect GPUs inside AI training clusters — and fewer than five companies worldwide manufacture them at commercial scale: Lumentum, Coherent, Mitsubishi, Sumitomo, and Broadcom.

On March 2, 2026, Nvidia committed $2 billion each to Lumentum and Coherent — a $4 billion lockup of EML laser supply — along with additional investments in Scintil Photonics and Ayar Labs, securing priority capacity and future access rights for advanced laser components. The combined commitment was explicitly aimed at locking in EML supply that Nvidia views as a structural bottleneck, and the result has been stark: lead times at key EML suppliers have stretched beyond 2027 for any buyer who is not Nvidia.

The lockup has forced optical module manufacturers and cloud service providers to search for secondary suppliers and alternative designs. The alternative path — continuous-wave lasers paired with silicon photonics chips — is itself under pressure. CW laser production faces long equipment delivery cycles and strict reliability standards requiring labor-intensive die-cutting and aging tests, causing that supply chain to approach a capacity crunch in parallel, according to TrendForce.

Why AI Data Centers Need 36 Times More Fiber Than Standard Racks

The laser crunch is matched by an equally severe shortage in optical fiber. AI-focused data centers need approximately 36 times more fiber than traditional CPU server racks, according to Rahul Puri, CEO of optical networking firm STL — a figure confirmed by Tom's Hardware reporting on the crisis. Data center fiber demand grew roughly 76% year-on-year in 2025, and the segment is projected to account for 30% of total global fiber demand by 2027, up from below 5% as recently as 2024.

The supply gap is stark. North American demand growth is projected at 22% to 25% in 2026, while supply expansion trails at 12% to 19%. Lead times have stretched to 20 weeks for large-volume buyers and up to a year for smaller purchasers. Manufacturing optical fiber preforms — the glass rods from which fiber is drawn — typically takes 18 to 24 months to expand, limiting near-term supply regardless of downstream investment.

The fiber shortage is not confined to data centers. The same supply crunch is squeezing the United States' $42.5 billion Broadband Equity, Access and Deployment program, which was designed to bring high-speed internet to roughly 8 million underserved rural homes. Anis Khemakhem, chief commercial officer at Clearfield, has described the collision of data center demand and BEAD rollout as making the shortage "more pronounced" than either force alone would produce — a view echoed by AT&T CEO John Stankey, who specifically cited supply chain constraints as a reason to doubt the industry's 110-million-home broadband expansion commitment would fully materialize.

Hyperscalers Lock In Supply With Billion-Dollar Agreements

Facing a market where availability — not price — has become the defining constraint, hyperscalers have moved to secure fiber supply through long-term agreements. Meta signed a $6 billion supply agreement with Corning in January 2026, and Corning also disclosed two additional deals of similar scale with unnamed hyperscalers in its Q1 2026 earnings. Nvidia separately invested $300 million in Corning to fund three new fiber manufacturing plants in North Carolina and Texas.

Japanese optical fiber maker Fujikura announced in March 2026 that it would invest up to 300 billion yen — approximately $1.88 billion — to triple production capacity across Japan and the United States, specifically citing rising AI data center demand and its designation as a key supplier for US AI infrastructure.

Chinese Suppliers Step In, With Constraints of Their Own

As US and Japanese vendors work to expand strained capacity, Chinese manufacturers have gained significant ground in module assembly. Innolight and Eoptolink — both incorporated in China — supply approximately 60% of Nvidia's 800G module demand, according to industry analysis by MLQ.ai and Photoncap.net. Seven of the top ten global optical module suppliers in 2024 were Chinese companies.

Chinese manufacturers hold structural advantages in assembly volume and cost, but face real limits on how far up the value chain they can climb. Export controls imposed by the United States, Japan, and the Netherlands restrict access to certain epitaxial growth equipment — including metal-organic chemical vapor deposition and molecular beam epitaxy systems — needed to scale production of higher-end components such as EMLs and DSP chips. Critical components thus remain concentrated among a small number of Western and Japanese suppliers with significant pricing power.

One legal condition applies to Chinese optical module suppliers regardless of product design: China's National Intelligence Law of 2017 obligates PRC-incorporated companies to cooperate with state intelligence requests. No confirmed data-access incident involving Innolight or Eoptolink has been reported; optical modules are physical hardware rather than data-collection software, and that distinction matters for risk assessment. The legal obligation nonetheless remains a structural condition for any enterprise buyer evaluating Chinese optical module suppliers.

What Fixes Are Coming — and Why They Take Years

Corning, Lumentum, and Coherent are all investing in expanded capacity, but optical component manufacturing does not scale quickly. Lumentum is currently the only supplier shipping 200-gigabit-per-lane EMLs at volume — the specific component required for next-generation 1.6T transceivers. Coherent operates a 6-inch indium phosphide wafer line in Sherman, Texas, representing one of the most advanced manufacturing steps in the supply chain.

The specialized indium phosphide fabrication required for EML lasers involves yields ranging from 15% to 50% depending on wafer generation and design complexity, according to McKinsey analysis. That range alone explains why capacity cannot simply be ordered into existence: even with substantial capital investment, yields must be qualified through extensive production runs before volume commitments can be met. Lumentum is investing in expanding its San Jose InP fabrication facility, while analysts expect double-digit price increases on 200G EMLs in 2026 given the absence of viable second-source suppliers.

LightCounting, the optical transceiver research firm, offered a somewhat more optimistic view in its January 2026 forecast, projecting that InP laser shortages would begin to ease by mid-2026 as new capacity comes online. The firm does not forecast a full cycle downturn but does flag the likelihood of a flat quarter or two in late 2026 as supply and demand find a new equilibrium.

The broader pattern mirrors what has played out repeatedly across the AI buildout: infrastructure designed for generational upgrades is being asked to scale at a pace set by software and capital, not physics and fabrication capacity. For AI clusters that cannot ship without optical interconnects, the laser chokepoint is as consequential as any GPU allocation — and significantly harder to resolve on a short timeline.

Frequently Asked Questions

Why are AI data centers causing an optical component shortage?

AI training clusters require roughly six high-speed optical transceivers per GPU — far more than conventional servers — because GPU-to-GPU connections must sustain far greater bandwidth across longer distances inside the cluster. As hyperscalers have scaled from single-rack to multi-rack configurations, demand for 800G transceivers jumped from 24 million units in 2025 to a projected 63 million in 2026, overwhelming manufacturing capacity that was never designed for this pace.

What is causing the optical transceiver shortage in 2026?

The core constraint is the electro-absorption modulated laser, a precision component manufactured by only a handful of companies globally. In March 2026, Nvidia committed $4 billion to Lumentum and Coherent to secure priority access to their EML production, pushing lead times for all other buyers beyond 2027. The alternative laser design — continuous-wave lasers paired with silicon photonics chips — is itself approaching capacity limits for similar reasons.

How long will the fiber optic cable shortage last?

McKinsey analysis projects 800G transceiver shortages will persist through 2027, and 1.6-terabit shortfalls are likely through 2029. For optical fiber specifically, new preform manufacturing capacity takes 18 to 24 months to build, meaning investments announced in 2025 and early 2026 will not meaningfully ease supply until late 2027 at the earliest.

Why did Nvidia invest in Lumentum and Coherent?

Nvidia invested $2 billion each in Lumentum and Coherent on March 2, 2026, to secure priority access and future capacity rights for the EML lasers needed for its next-generation silicon photonics networking products. The investments include multibillion-dollar purchase commitments and signal that Nvidia views the photonics supply chain as a structural bottleneck for AI infrastructure scaling — one that cannot be resolved through purchase orders alone.

ⓒ 2026 TECHTIMES.com All rights reserved. Do not reproduce without permission.